전설적인 투자자가인 하워드 막스가 작금에 상전벽해급 변화가 일어나고 있다는 주장을 하면서 관심을 받고 있습니다. 너무도 엄청난 변화라 기존의 투자 전략이 전혀 먹혀들지 않은 시간이 왔다고 주장하고 있습니다.

투자의 구루로 추앙받는 하워드 막스는 1970년대부터 투자를 시작해서 지금까지 53년을 주식 투자 분야에서 전설적인 실적을 쌓은 사람입니다.

그 장구한 시기 동안 하워드 막스는 딱 3번의 상전벽해급 변화(sea change)를 목격했는데 그 중 하나가 지금 우리 앞에서 전개되고 있는 상황이라고 주장합니다.

A sea change is under way in markets

투자 세계에서 53년 동안, 저는 여러 번의 경기 순환(economic cycles), 진자의 흔들림(pendulum swings), 거품과 붕괴(bubbles and crashes)를 보았지만, 저는 단지 두 번의 실제 상전벽해 변화(real sea changes)를 기억합니다. 내 생각에 우리는 오늘 세 번째 상전벽해 변화 중에 있을지도 모릅니다.

첫 번째 상전벽해 변화는 1970년대에 고수익 채권이 생기면서 발생했습니다.

197년대 고수익 채권(high-yield bonds) 시대 개막

첫 번째는 1970년대에 고수익 채권(high-yield bonds)이 생기면서 발생했습니다.

신중한 채권 투자(Prudent bond investing)는 이전에는 안전한 것으로 추정되는 투자 등급 채권만 사는 것으로 구성되었습니다. 하지만 투자 관리자들은 이제 부수적인 위험을 적절히 보상받는 한 거의 모든 품질의 채권을 신중하게 살 수 있습니다.

이것은 새로운 투자 심리를 반영했습니다. 이제 위험은 피할 필요가 없고, 오히려 수익에 상대적인 것으로 여겨졌고, 현명하게 대처하기를 바랍니다.

이러한 새로운 리스크/리턴(risk/return) 사고방식은 사모펀드(private equity), 부실채권(distressed debt), 주택담보대출 증권(mortgage-backed securities), 구조화된 신용 및 민간 대출(structured credit and private lending)과 같은 많은 새로운 유형의 투자를 개발하는 데 중요했습니다.

오늘날의 투자 세계는 50년 전과 거의 닮지 않았다고 해도 과언이 아니다.

장기적인 금리하락 시대

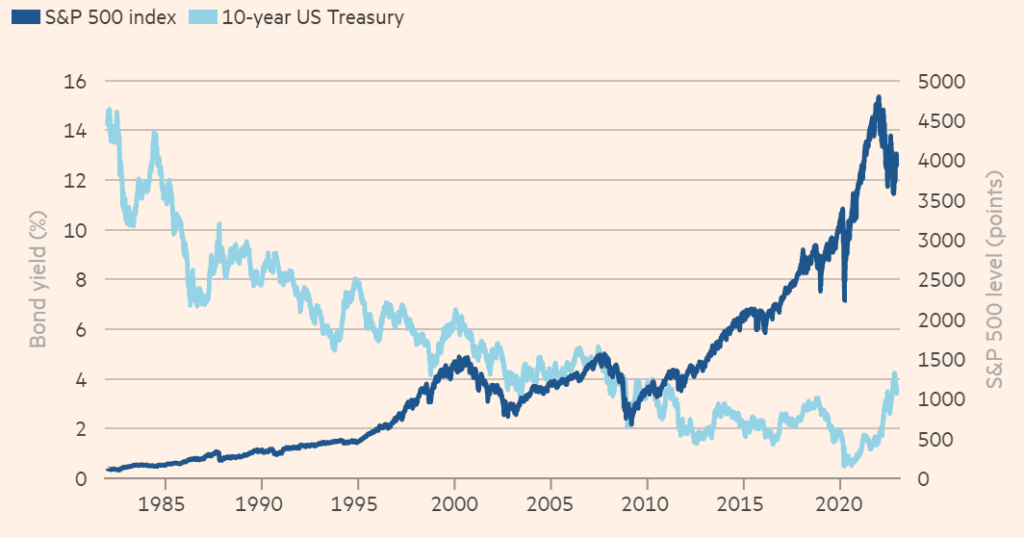

그 다음으로 큰 변화는 장기적인 금리 하락(the long-term decline in interest rates)이었습니다.

이러한 추세는 리스크/리턴(risk/return) 사고가 등장한 지 불과 몇 년 후에 시작되었으며, 저는 이 두 가지의 조합이 1980년대 초에 시작된 40년간의 놀라운 주식 시장 성과를 크게 만들었다고 생각합니다.

S&P 500 지수는 1982년 8월 102에서 2022년 초 4,796으로 상승하여 연간 10.3%의 복리 연간 수익률(a compound annual return)을 기록했습니다.

분명히 이 기간 동안 미국의 경제 성장, 미국의 위대한 기업들의 실적, 기술, 생산성 및 관리 기술의 향상, 세계화의 이점을 포함하여 여러 가지 요인이 투자자들의 성공을 초래했습니다. 하지만, 40년 동안의 금리 하락이 가장 큰 역할을 하지 못했다면 저는 놀랄 것입니다.

이전 변화를 부정하는 새로운 변화

물론, 위의 모든 것들은 작년에 뒤집혔습니다.

가장 중요한 것은 2021년 초에 고개를 들기 시작한 인플레이션으로 인해 연방준비제도이사회는 2022년에 기록상 가장 빠른 금리 인상 사이클 중 하나를 시작했습니다.

그 결과, 손쉬운 돈과 낙관적인 대출자와 자산 소유자로 특징지어지는 시장이 사라졌습니다.

갑자기, 대출자와 구매자가 더 나은 카드를 갖게 되었습니다.

Oaktree와 같은 신용 투자자들은 더 높은 수익률과 더 강력한 채권자 보호를 요구할 수 있는 더 나은 위치에 놓이게 되었습니다.

곤경에 처한 수준에서 거래되는 대출 및 채권 목록은 수십 개에서 수백 개로 증가했습니다.

간단히 말해서, 그것은 지난 40년의 대부분을 지배했던 상황을 완전히 뒤집은 것처럼 보였습니다.

제가 보기에 S&P 500 지수의 최근 10% 상승을 이끌었던 매수자들은 경제와 시장이 이전 시대의 Halcyon 시대(이전 시대의 침체기)로 돌아갈 것이라는 믿음에서 시작되었습니다.

그들은 인플레이션이 완화되고 있고, 연준이 곧 피봇하여 금리를 인하하고 경기 침체를 피할 것이라고 생각합니다. 하지만 이러한 믿음들이 정당한가요?

제가 경제와 시장에 대해 여러 번 썼듯이, 우리는 우리가 어디로 가고 있는지 결코 알지 못하지만, 우리는 우리가 어디에 있는지 알아야 합니다.

작금의 상황은 매우 달라졌고 비우호적인 상황, 이전 투자전략은 먹히지 않는 시대

결론은, 많은 면에서, 지금 이 순간의 상황은 금융 위기 이후와 압도적으로 다르고, 대부분 호의적이지 않다는 것입니다.

이러한 변화는 오래 지속되거나 시간이 지남에 따라 사라질 수 있습니다.

하지만 제가 보기에는 2009년 이후 특징이었던 것과 같은 낙관적이고 쉬운 상황으로 빠르게 돌아오는 것을 볼 수 없을 것 같습니다.

우리는 2009-21년의 낮은 수익률의 세계(the low-return world)에서 완전한 수익률의 세계(a full-return world)로 이동했습니다.

이제 투자자들은 잠재적으로 신용 상품으로부터 확실한 수익을 얻을 수 있습니다. 즉, 전반적인 수익 목표를 달성하기 위해 더 이상 위험한 투자에 크게 의존할 필요가 없습니다.

대출자와 바겐세일 사냥꾼은 2009-21년보다 이 변화된 환경에서 훨씬 더 나은 전망에 직면해 있습니다.(Lenders and bargain hunters face much better prospects in this changed environment than they did in 2009-21.)

그리고 중요한 것은 환경이 지난 13년 동안 그리고 대부분의 지난 40년 동안과 매우 다르다는 것을 인정한다면, 그 기간 동안 가장 잘 작동했던 투자 전략이 앞으로 몇 년 동안 더 이상 성과를 내지 못할 수도 있다는 것입니다. (the investment strategies that worked best over those periods may not be the ones that outperform in the years ahead.)

그것이 제가 말하는 변화입니다.

컬럼 원문

In my 53 years in the investment world, I’ve seen a number of economic cycles, pendulum swings, bubbles and crashes, but I remember only two real sea changes. I think we may be in the midst of a third one today.

The first occurred in the 1970s with the creation of high-yield bonds. Prudent bond investing had previously consisted of buying only presumedly safe investment grade bonds. But investment managers could now prudently buy bonds of almost any quality as long as they were adequately compensated for the attendant risk.

This reflected a new investor mentality. Now risk wasn’t necessarily avoided, but rather considered relative to return and hopefully borne intelligently. This new risk/return mindset was critical in the development of many new types of investment, such as private equity, distressed debt, mortgage-backed securities, structured credit and private lending. It’s no exaggeration to say today’s investment world bears almost no resemblance to that of 50 years ago.

The next big change was the long-term decline in interest rates. This trend began just a few years after the advent of risk/return thinking and I believe the combination of the two largely gave rise to the incredible four decades of stock market performance that began in the early 1980s. The S&P 500 index rose from a low of 102 in August 1982 to 4,796 at the beginning of 2022, for a compound annual return of 10.3 per cent per year.

Obviously, multiple factors gave rise to investors’ success over this period, including economic growth in the US; the strong performance of the country’s greatest companies; gains in technology, productivity and management techniques; and the benefits of globalisation. However, I’d be surprised if 40 years of declining interest rates didn’t play the greatest role of all.

Of course, all of the above flipped in the last year. Most importantly, inflation, which began to rear its head in early 2021, caused the Federal Reserve to kick off one of the quickest rate-hiking cycles on record in 2022. As a result, the market characterised by easy money and optimistic borrowers and asset owners disappeared; suddenly, lenders and buyers held better cards. Credit investors like Oaktree became better positioned to demand higher returns and stronger creditor protections. The list of loans and bonds trading at distressed levels grew from dozens to hundreds.

In short, it looked like a complete reversal of the conditions that prevailed for much of the last 40 years.

In my view, the buyers who’ve driven the S&P 500’s recent 10 per cent rally from the October low have been motivated by a belief that the economy and markets will return to the halcyon days of this previous era. They appear to think that inflation is easing, the Fed will soon pivot and reduce interest rates and a recession will be averted, or be modest and brief. But are these beliefs justified?

As I’ve written many times about the economy and markets, we never know where we’re going, but we ought to know where we are. The bottom line for me is that, in many ways, conditions at this moment are overwhelmingly different from — and mostly less favourable than — those of the post-financial crisis climate. These changes may be long-lasting, or they may wear off over time. But in my view, we’re unlikely to see a quick return of the same optimism and ease that marked the period after 2009.

We’ve gone from the low-return world of 2009-21 to a full-return world. Investors can now potentially get solid returns from credit instruments, meaning they no longer have to rely as heavily on riskier investments to achieve their overall return targets.

Lenders and bargain hunters face much better prospects in this changed environment than they did in 2009-21. And, importantly, if you grant that the environment is and may continue to be very different from what it was over the past 13 years — and most of the last 40 years — it should follow that the investment strategies that worked best over those periods may not be the ones that outperform in the years ahead. That’s the sea change I’m talking about.